For decades, applying for a loan meant walking into a bank, filling out paperwork, and waiting—sometimes anxiously—for a decision that seemed to depend almost entirely on a three-digit credit score. Upstart was built around the idea that this system leaves too many people behind. Instead of relying only on traditional credit models, the platform aims to evaluate borrowers more holistically and deliver faster, more streamlined access to funding.

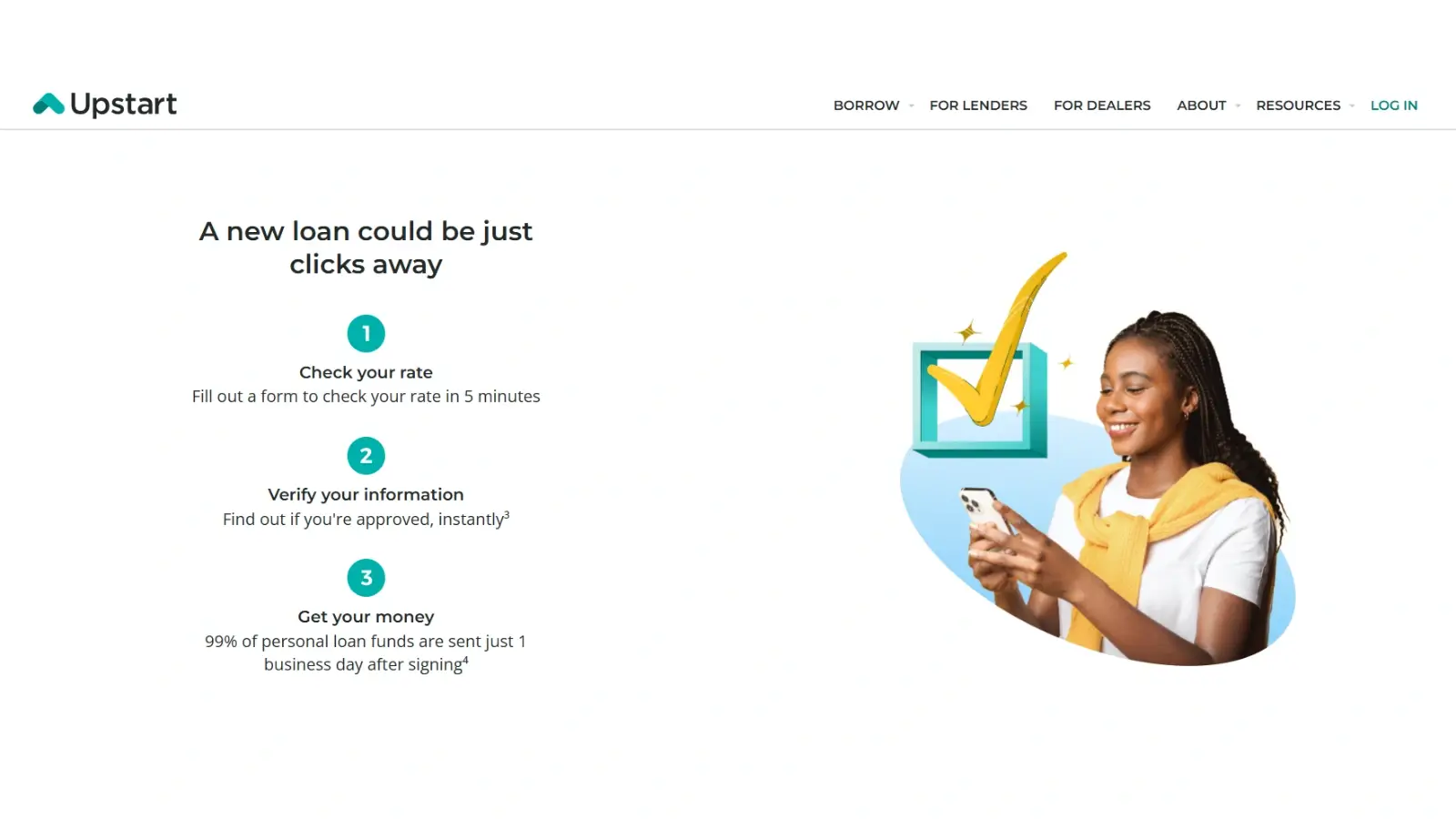

Founded in 2012, Upstart positions itself as a technology company first and a lending marketplace second. It partners with banks and credit unions that actually fund the loans, while its proprietary platform handles the application process and risk assessment. For consumers, the experience is simple: complete an online form, receive potential loan offers, review the terms, and accept if the conditions make sense. In many cases, approved funds are sent quickly, sometimes as soon as the next business day.

What makes Upstart different is the way it assesses risk. Traditional lenders focus heavily on credit scores and past borrowing history. Upstart’s model incorporates additional variables such as education, employment background, and income patterns. By analyzing a wider range of data points, the platform attempts to predict creditworthiness more accurately than conventional models alone. The goal is to approve more qualified borrowers at fair rates while keeping default risk in check for partner institutions.

This approach has drawn significant attention in the financial technology space. Supporters argue that it creates opportunity for individuals who may not have a long credit history but demonstrate strong earning potential or financial stability. For example, a recent graduate with a solid job offer but limited credit activity might receive better consideration through Upstart’s system than through a traditional bank’s rigid scoring framework. Critics, however, note that algorithm-driven lending must be carefully monitored to ensure fairness and transparency.

Upstart’s primary product is personal loans, often used for consolidating credit card balances, covering medical expenses, or handling unexpected financial needs. Debt consolidation is one of the most common uses. Borrowers combine multiple high-interest balances into one fixed monthly payment, ideally at a lower rate. This can simplify finances and potentially reduce the total cost of repayment over time. Similarly, Yup Loans personal loans focus on a quick online application that can match you with lenders who look beyond just a credit score, with decisions often delivered fast and funding potentially as soon as the next business day.

In addition to personal loans, Upstart has expanded into car loan refinancing and other credit solutions. By working with established banks and credit unions, the company avoids acting as a traditional lender that holds loans long term. Instead, it earns fees for originating and servicing loans through its technology platform. This asset-light model allows Upstart to focus on refining its algorithms and scaling its partnerships.

The online experience is central to the brand. The application is designed to be straightforward, with clear disclosures and transparent rate information before a borrower commits. There is no obligation to accept a loan offer simply by checking rates, which gives users space to compare options. Interest rates vary depending on individual risk profiles, market conditions, and the specific partner institution funding the loan. As with any financial decision, borrowers are encouraged to review the annual percentage rate, fees, and repayment terms carefully.

Upstart’s growth has not been without volatility. Like many fintech companies, it is sensitive to changes in interest rates and broader economic conditions. When borrowing costs rise or investor appetite for loans tightens, lending activity can slow. Nevertheless, the company continues to refine its underwriting model and expand its network of financial partners.

At a broader level, Upstart reflects a shift in how financial services are delivered. Consumers increasingly expect digital convenience, rapid decisions, and personalized experiences. By combining data analytics with a marketplace model, Upstart represents one attempt to modernize credit access without entirely replacing traditional banks.

For borrowers, the real question is practical: does it provide a competitive, transparent, and manageable loan option? For many users, the answer has been yes, particularly when speed and accessibility matter most. As technology continues to reshape finance, platforms like Upstart will likely remain part of the evolving conversation about how credit is evaluated and distributed in the modern economy.

Business Outstanders brings you sharp insights on tech, business, entrepreneurship, law, crypto, and more. We uncover what’s next. Stay updated, sign up for our newsletter and be part of the future!